Introduction

In the ever-evolving business landscape, maximizing returns on capital employed is crucial to sustainable growth and success.

Return on Capital Employed (ROCE) is a valuable metric that measures the profitability and efficiency of a company’s capital investments.

In this article, we will delve into the significance of ROCE, its calculation, factors affecting it, strategies to improve it, and its limitations. By understanding and optimizing ROCE, businesses can enhance their financial performance and gain a competitive edge.

Understanding Return on Capital Employed (ROCE)

ROCE offers valuable insights into a company’s efficiency and profitability. Businesses can better understand their performance by analyzing the ROCE ratio over different periods or against industry benchmarks.

This analysis helps identify areas for improvement, such as streamlining operations, reducing unnecessary costs, or optimizing asset utilization.

Companies can increase their ROCE and generate higher returns for their stakeholders by implementing targeted strategies to enhance efficiency and profitability.

Calculating Return on Capital Employed (ROCE calculation)

To calculate ROCE, one divides the company’s operating profit (earnings before interest and taxes) by the capital employed and multiplies the result by 100 to express it as a percentage. The ROCE formula is as follows:

ROCE = (Operating Profit / Capital Employed) x 100

Where:

Operating Profit = Gross Profit – Operating Expenses

Operating profit represents a company’s earnings before accounting for interest and taxes, while capital employed encompasses the total value of long-term debt and shareholders’ equity.

By considering both aspects, ROCE provides a holistic assessment of the profitability and efficiency of a company’s capital investments.

Interest payments are excluded from the calculation of operating profit (also known as earnings before interest and tax, or EBIT) because they represent costs that a business cannot directly control. Since a company cannot set its interest rates, it is considered a separate component and is removed from the operating profit calculation. By focusing solely on the aspects of the business that it can control, operating profit provides a more accurate measure of the company’s profitability and efficiency.

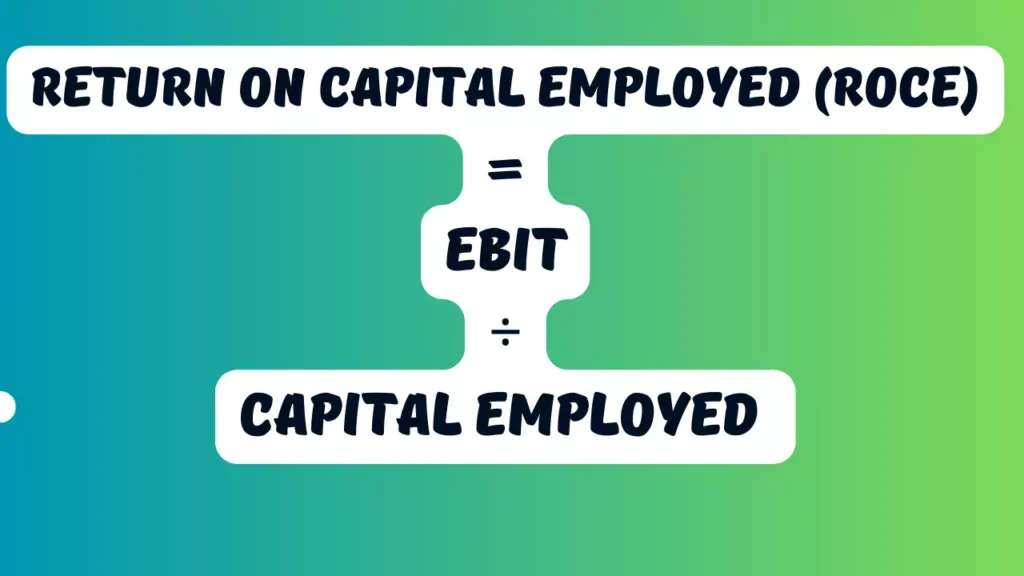

Another way to calculate is by using the ROCE formula:

ROCE = EBIT / Capital Employed

Where:

- EBIT (Earnings before interest and taxes ) = Revenue – COGS (Cost of goods sold) – Operating expenses

- Capital Employed = Total assets – Total current liabilities or

- Capital employed = Equity + Non-current Liabilities

- Capital employed = Shareholders’ Equity + Non-Current Liabilities

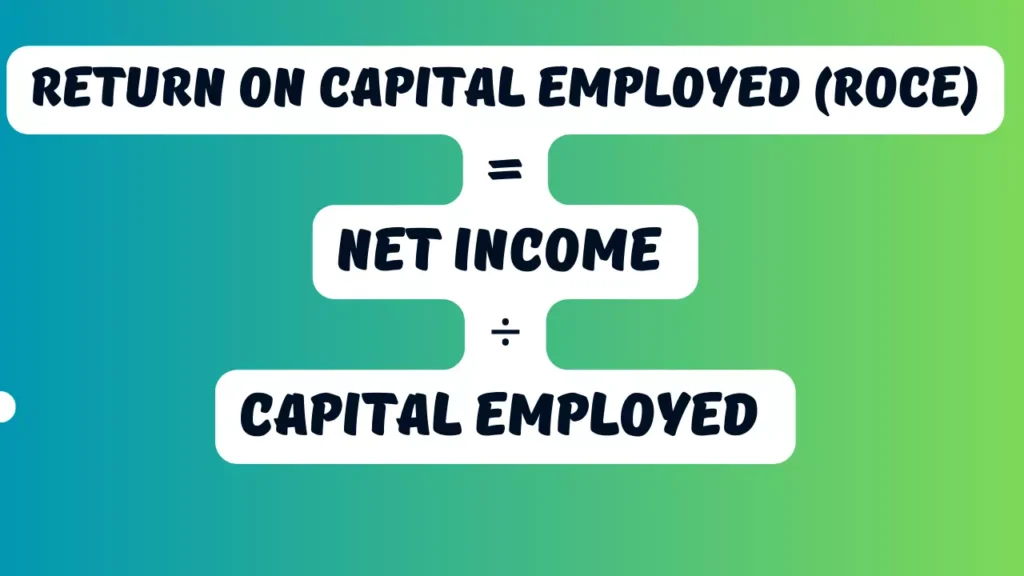

Alternatively, ROCE calculation using the ROCE formula:

ROCE = Net income / Capital Employed

Where:

- Net income = profit after taxes

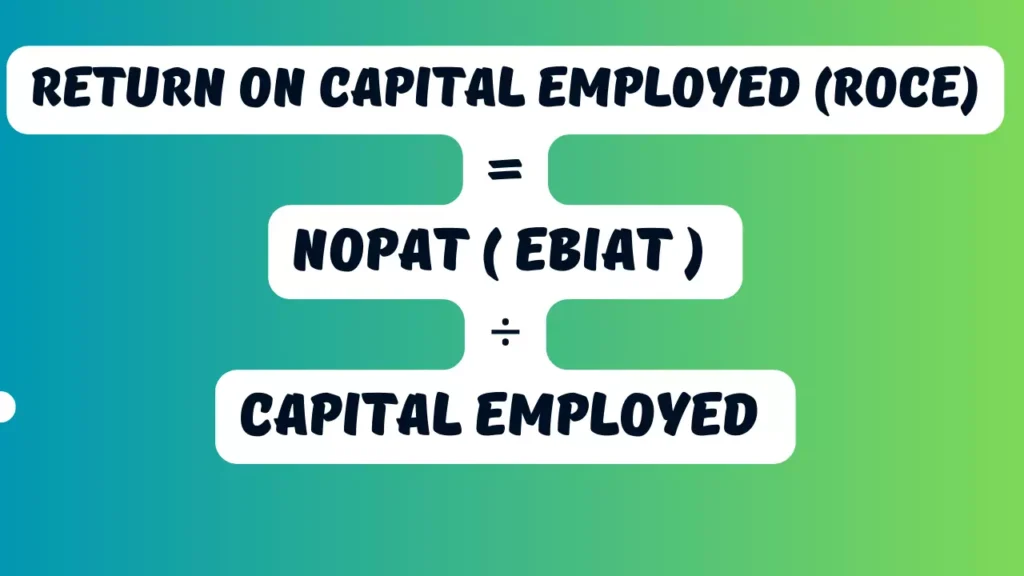

The Other way to calculate Return on Capital Employed (ROCE):

Return on Capital Employed (ROCE) = NOPAT ( EBIAT ) ÷ Capital Employed

Where:

- NOPAT (operating profit after taxes) = EBIT × (1 – Tax Rate %)

In contrast, some variations of ROCE utilize operating income (EBIT) instead of net operating profit after taxes (NOPAT) in the numerator.

The rationale behind using EBIT is that taxes, which represent profits paid out and are not available to financiers, should be excluded to obtain a more accurate measure of capital efficiency.

By focusing on operating income, the metric aims to reflect the profitability generated solely from the business’s core operations.

However, it is worth noting that the choice between EBIT and NOPAT in the calculation of ROCE is unlikely to impact the overall result significantly.

Both versions provide insights into the company’s ability to generate returns on its capital employed.

This metric aims to reflect the profitability generated solely from the business’s core operations by focusing on operating income.

Real-Life Examples and Interpretation of Return on Capital Employed in Indian Stocks

Let’s look at some examples of Return on Capital Employed in Indian stocks and interpret their implications:

ITC: ITC has a ROCE of 32.6%, which is very high. It means that for every 100 rupees invested in ITC, the company generates 32.6 rupees of profit.

HDFC Bank: HDFC Bank has a Return on Capital Employed of 22.5%, which is also considered very high. It means that for every 100 rupees invested in HDFC Bank, the company generates 22.5 rupees of profit.

Tata Steel: Tata Steel has an average Return on Capital Employed of 12.2%. It means that for every 100 rupees invested in Tata Steel, the company generates 12.2 rupees of profit.

Infosys: Infosys has a Return on Capital Employed of 20.2%, which is considered to be good. It means that for every 100 rupees invested in Infosys, the company generates 20.2 rupees of profit.

It is important to note that Return on Capital Employed can vary significantly between different industries. For example, a company in the financial services industry is likely to have a higher ROCE than a company in the manufacturing industry.

Financial services companies typically have significant intangible assets, such as intellectual property, which can generate high returns.

When interpreting Return on Capital Employed, it is also important to consider the company’s track record. A company with a consistently high ROCE will likely be a good investment, as it will likely continue generating high returns.

However, a company with a low Return on Capital Employed suddenly showing a high Return on Capital Employed may indicate accounting irregularities.

Interpreting ROCE Ratios

Interpreting ROCE ratios requires careful analysis and consideration of the company’s industry, business model, and capital structure.

A high ROCE ratio is generally considered favourable as it signifies that a company generates significant returns from its capital investments. However, a high ratio only sometimes guarantees sustained success.

Factors such as industry dynamics, competitive pressures, and changing market conditions can influence the interpretation of ROCE ratios. Examining trends, benchmarking against industry peers, and conducting a comprehensive analysis before concluding is crucial.

Industry Benchmarking and Competitive Analysis

Benchmarking ROCE against industry peers is an effective way to assess a company’s competitive position.

By comparing ROCE ratios within the same industry, businesses can identify the leaders in capital efficiency and learn from their strategies.

Benchmarking enables companies to set realistic performance targets, uncover best practices, and implement improvements to achieve a competitive advantage. However, it is important to consider industry-specific factors, such as variations in capital intensity or business cycles, to ensure accurate and meaningful comparisons.

Limitations of Return on Capital Employed

Let’s explore the limitations of ROCE and highlight considerations to enhance its effectiveness in evaluating financial performance.

Limitation 1: Ignoring the Timing of Cash Flows

One significant limitation of Return on Capital Employed is its failure to account for the timings of cash flows. ROCE focuses on overall profitability and capital efficiency but does not consider when cash flows occur.

Companies may have high ROCE ratios but face challenges if cash flows are delayed or unevenly distributed.

The timings of cash inflows and outflows can impact a company’s liquidity, working capital management, and financial health, aspects that are not captured by ROCE alone.

Limitation 2: Lack of Risk Consideration

ROCE also has limitations in its ability to incorporate risk considerations explicitly. While ROCE provides insights into the profitability of capital employed, it does not account for the risks associated with the invested capital.

Companies with higher ROCE may also face higher levels of risk, such as market volatility, regulatory changes, or technological disruptions.

And it is important to assess risk-adjusted returns by integrating metrics like,

- Risk-Adjusted Return on Capital (RAROC) or

- Economic Value Added (EVA).

To make well-informed investment decisions.

Limitation 3: Industry Variations

Return on Capital Employed may have limitations when comparing companies across different industries. Each industry has its unique dynamics, capital requirements, and business models.

For example, industries with heavy capital investments, like manufacturing or energy, may have lower ROCE ratios than those with lower capital requirements, such as technology or service-based sectors.

Comparing ROCE ratios without considering these industry-specific variations can lead to inaccurate conclusions.

Limitation 4: Macro Factors and External Influences

ROCE analysis may not capture the full impact of macroeconomic factors and external influences on a company’s performance.

Factors like changes in interest rates, government policies, or geopolitical events can significantly affect a company’s profitability and capital efficiency.

ROCE ratios provide insights into internal performance but do not consider the broader economic or environmental factors that can impact a company’s financial performance.

Limitation 5: Incomplete Picture of Performance

ROCE alone does not provide a comprehensive picture of a company’s financial performance. It focuses primarily on capital efficiency and profitability but overlooks other important aspects such as revenue growth, cash flow generation, and balance sheet strength.

And to get a holistic view of a company’s financial health and prospects, it is essential to analyze ROCE in conjunction with other financial metrics, such as revenue growth rates, free cash flow generation, debt levels, and return on equity (ROE).

Overcoming Limitations: Supplementary Metrics

Also, it is essential to consider supplementary metrics to overcome the limitations of ROCE and gain a more comprehensive perspective on a company’s financial performance. These metrics can provide additional insights and complement the analysis of Return on Capital Employed. Here are some metrics that can be used:

Cash Flow Analysis

Assessing the timing and magnitude of cash flows provides insights into a company’s liquidity, working capital management, and ability to meet financial obligations.

Cash flow analysis complements Return on Capital Employed by considering the cash inflows and outflows associated with a company’s operations, investments, and financing activities.

By analyzing cash flow patterns, companies can identify areas for improvement, optimize working capital, and ensure sustainable profitability.

Risk-Adjusted Return Measures

Incorporating risk considerations is crucial to gain a more accurate assessment of a company’s financial performance.

Metrics such as Risk-Adjusted Return on Capital (RAROC) or Economic Value Added (EVA) consider the risk associated with capital employed.

These measures help adjust Return on Capital Employed for the level of risk undertaken by the company.

By incorporating risk-adjusted metrics, companies can evaluate the profitability of their investments in light of the associated risks, enabling more informed decision-making.

Comparative Industry Analysis

Comparative industry analysis allows companies to benchmark their financial performance against industry-specific benchmarks and ratios.

By comparing Return on Capital Employed ratios within the same sector, businesses can gain insights into their competitive position and identify areas for improvement.

The comparative analysis considers industry-specific dynamics, capital requirements, and performance benchmarks to evaluate a company’s financial performance better.

Balanced Scorecards

Implementing balanced scorecards offers a holistic approach to evaluating a company’s overall performance and strategic alignment.

Balanced scorecards incorporate multiple financial and non-financial metrics to assess a company’s performance comprehensively.

By considering metrics related to financial performance, customer satisfaction, internal processes, and learning and growth, balanced scorecards offer a more well-rounded view of a company’s performance and potential areas for improvement.

ROCE in Different Business Contexts

ROCE holds importance in various industries as it serves as a performance benchmark and aids in evaluating capital efficiency and profitability.

By understanding the specific dynamics of each industry, we can explore how ROCE applies and influences decision-making.

ROCE in Manufacturing Industry

In the manufacturing industry, Return on Capital Employed helps assess the effectiveness of capital investments in production facilities, equipment, and supply chain management.

By measuring ROCE, manufacturing companies can evaluate the efficiency of their operations, optimize asset utilization, and improve overall profitability.

Return on Capital Employed is particularly useful for manufacturers with high capital requirements and long production cycles.

ROCE in Retail Industry

For retailers, ROCE is crucial in evaluating the profitability and efficiency of their store networks, inventory management, and working capital utilization. It helps retailers identify underperforming stores, optimize their product mix, and streamline their supply chain.

Return on Capital Employed aids in identifying the most profitable retail formats, such as brick-and-mortar stores, e-commerce platforms, or a combination of both.

ROCE in Technology Industry

In the fast-paced technology industry, ROCE is a performance indicator for evaluating investments in research and development, intellectual property, and technological infrastructure. Technology companies rely heavily on innovation and capital investments to drive growth.

ROCE allows them to assess the success of their assets, make strategic decisions regarding product development, and allocate resources effectively.

ROCE in Financial Services Industry

In the financial services industry, ROCE is vital in assessing the profitability and effectiveness of capital deployed in banking operations, insurance underwriting, asset management, and other economic activities.

Financial institutions utilize Return on Capital Employed to evaluate the returns from lending activities, investment portfolios, and capital-intensive operations. It helps them make informed decisions regarding business expansion and risk management.

ROCE in Energy Industry

The energy industry heavily relies on capital-intensive projects, encompassing oil and gas, renewable energy, and utilities. ROCE helps evaluate the efficiency and profitability of these investments, such as oil exploration and production, renewable energy infrastructure, and power generation facilities.

By measuring ROCE, energy companies can assess the long-term viability of their projects, optimize capital allocation, and maintain sustainable profitability.

ROCE in Healthcare Industry

In the healthcare sector, ROCE aids in evaluating the performance of hospitals, pharmaceutical companies, medical device manufacturers, and healthcare service providers.

Return on Capital Employed is particularly relevant in assessing the profitability of investments in medical equipment, research and development, and healthcare facilities.

It assists companies in optimizing capital utilization, enhancing operational efficiency, and delivering quality patient care.

ROCE in Construction Industry

The construction industry relies heavily on capital investments in infrastructure projects, real estate development, and construction equipment.

ROCE allows construction companies to measure the effectiveness of their capital allocations, optimize project selection, and manage risks.

By evaluating Return on Capital Employed, construction firms can identify profitable projects, control costs, and improve overall project profitability.

ROCE in Telecommunications Industry

In the telecommunications sector, ROCE is essential for evaluating investments in network infrastructure, spectrum licenses, and technology upgrades.

It helps telecom companies assess the profitability of their capital-intensive operations, optimize network utilization, and make strategic decisions regarding network expansion and service offerings. ROCE assists in evaluating the financial viability of investments in the rapidly evolving telecommunications landscape.

ROCE in Automotive Industry

For automotive manufacturers, ROCE is instrumental in evaluating investments in production facilities, research and development, and product innovation.

It helps companies assess the efficiency of their capital utilization, optimize supply chain management, and improve profitability.

Return on Capital Employed aids automotive companies in making strategic decisions related to product portfolios, manufacturing processes, and global expansion.

ROCE in Hospitality Industry

ROCE measures profitability and capital efficiency for hotels, resorts, and hospitality service providers in the hospitality sector.

It assists in assessing the effectiveness of capital investments in property development, customer experience enhancement, and revenue generation.

By evaluating Return on Capital Employed, hospitality companies can optimize pricing strategies, improve cost management, and enhance guest satisfaction to maximize returns on their capital investments.

ROCE in Pharmaceutical Industry

In the pharmaceutical industry, ROCE helps evaluate investments in research and development, manufacturing capabilities, and intellectual property.

It aids pharmaceutical companies in assessing the profitability and efficiency of their drug pipelines, optimizing resource allocation, and making strategic decisions regarding product portfolios.

ROCE assists in evaluating the returns from capital-intensive activities within the pharmaceutical value chain.

Enhancing ROCE: Strategies and Best Practices

To improve ROCE, companies can implement various strategies and best practices tailored to their specific business context. Here are some approaches to enhance Return on Capital Employed:

Operational Efficiency

Improving operational efficiency is crucial to increasing ROCE. Companies can optimize their processes, reduce waste, and streamline operations to enhance productivity and profitability.

It can involve implementing lean manufacturing principles, investing in automation and technology, and adopting efficient supply chain management practices.

Companies can maximize their capital utilization and generate higher returns by continuously seeking operational improvements.

Working Capital Management

Efficient working capital management is essential for enhancing ROCE. Companies can optimize their cash conversion cycle by reducing inventory levels, improving accounts receivable and accounts payable processes, and managing working capital requirements effectively.

By minimizing the cash tied up in working capital, businesses can improve their liquidity position and generate higher returns on their invested capital.

Capital Expenditure Optimization

Strategic capital expenditure optimization is key to improving ROCE. Companies can evaluate their investment projects rigorously, focusing on those with higher expected returns and aligning them with their overall business strategy.

It involves conducting thorough feasibility studies, risk assessments, and financial modelling to ensure that capital investments generate satisfactory returns. By allocating capital to projects with higher profitability potential, companies can enhance their overall Return on Capital Employed.

Pricing Strategy

Developing a robust pricing strategy is crucial for improving Return on Capital Employed. Companies must evaluate their pricing models, considering factors such as production costs, competitive dynamics, customer preferences, and value proposition.

By optimizing pricing strategies, businesses can increase their profitability, improve their margins, and generate higher returns on their capital employed.

Asset Utilization and Efficiency

Optimizing asset utilization and efficiency can significantly impact ROCE. Companies should regularly assess their asset base, identifying underutilized or obsolete assets that can be divested or repurposed.

By maximizing the utilization of assets, companies can generate higher revenues and improve their capital efficiency, leading to improved Return on Capital Employed.

Debt Management

Effective debt management is crucial for enhancing ROCE. Companies need to evaluate their capital structure, optimizing the mix of debt and equity to minimize financing costs and maximize returns.

It involves refinancing high-cost debt, negotiating favourable terms with lenders, and maintaining a balanced capital structure that aligns with the company’s risk profile.

By managing debt effectively, companies can improve their financial performance and Return on Capital Employed.

Capital Allocation Decisions and ROCE

Capital allocation decisions play a vital role in determining a company’s ROCE. Companies must rigorously evaluate investment opportunities, considering their potential impact on ROCE and overall profitability.

Risk-adjusted returns, industry dynamics, competitive advantage, and strategic alignment should be considered when allocating capital.

By prioritizing investments with higher expected returns and aligning them with the company’s strategic objectives, businesses can improve their ROCE and create long-term shareholder value.

Evaluating Investment Opportunities with ROCE

ROCE serves as a valuable tool for evaluating investment opportunities. When assessing potential investments, companies can analyze the expected impact on ROCE, considering factors such as projected cash flows, capital requirements, and associated risks.

Investments expected to generate higher returns and improve ROCE can be prioritized, while those with lower expected returns or higher risks may be re-evaluated.

By incorporating Return on Capital Employed analysis into the investment evaluation process, companies can make more informed decisions and allocate capital more effectively.

Financial Shenanigans: Manipulating ROCE

Companies may use financial shenanigans to manipulate financial statements and misrepresent their health. Here are some tactics that can artificially inflate or deflate ROCE:

Inflating Operating Profit

One method to manipulate ROCE is by inflating the reported operating profit. Companies may engage in aggressive revenue recognition practices, such as prematurely recording revenue or recognizing fictitious sales.

Similarly, they may understate expenses or use creative accounting techniques to overstate operating profit artificially.

Artificially Reducing Capital Employed

Another approach to manipulate ROCE is by artificially reducing the reported capital employed. Companies may use off-balance-sheet financing or complex financial instruments to hide debt or inflate equity.

By understating capital employed, companies can present a higher ROCE figure, which may mislead investors about the true financial health of the business.

Manipulating Depreciation and Amortization

Companies can also manipulate Return on Capital Employed by manipulating depreciation and amortization figures. They may extend the useful life of assets or use accelerated depreciation methods to reduce depreciation expense artificially.

By understating depreciation and amortization, companies can overstate the reported operating profit and inflate ROCE.

Misclassifying Expenses and Revenue

Misclassifying expenses and revenue is another tactic used to manipulate ROCE. Companies may shift expenses to different periods or misclassify them as capital expenditures to inflate current-period profits.

Similarly, they may defer revenue recognition or engage in revenue manipulation techniques to present a distorted picture of profitability and ROCE.

These financial shenanigans highlight the importance of conducting thorough due diligence and being aware of potential red flags when analyzing a company’s Return on Capital Employed. Let’s explore some warning signs investors should watch out for.

Red Flags to Watch for in ROCE Analysis

While analyzing ROCE, it is essential to be vigilant and identify any red flags that may indicate potential financial irregularities or challenges. Here are some red flags to consider when evaluating a company’s ROCE:

Unexplained ROCE Fluctuations

Significant and unexplained fluctuations in ROCE should raise concerns. Sharp increases or decreases in ROCE without any valid explanation may indicate manipulation or other underlying issues within the company’s financial statements.

ROCE Significantly Higher Than Industry Peers

If a company’s Return on Capital Employed is consistently and significantly higher than its industry peers, it may cause suspicion. While outperformance is possible, it is crucial to investigate further and determine the reasons behind the unusually high ROCE to ensure it is not a result of manipulation or unsustainable practices.

Negative ROCE or Consistently Low ROCE

Negative or consistently low ROCE can be a warning sign, indicating financial distress or inefficiency in capital utilization. Companies with negative ROCE may struggle to generate profits from their investments and face challenges sustaining their operations.

Inconsistent ROCE Compared to Net Income Growth

Inconsistencies between ROCE and net income growth rates should be scrutinized. If a company’s net income grows steadily, but the Return on Capital Employed remains stagnant or declines, it may suggest a mismatch between reported profits and the efficient utilization of capital.

Lack of Reinvestment in the Business

Companies that consistently report high profits but fail to reinvest in the business may indicate a red flag. If a company does not allocate sufficient capital towards research and development, innovation, or asset expansion, it may hinder long-term growth prospects and ROCE sustainability.

Excessive Debt Levels

High levels of debt can negatively impact ROCE. Excessive debt burdens can lead to increased interest expenses and reduced profitability, ultimately affecting ROCE. It is crucial to evaluate a company’s debt-to-equity ratio and overall leverage when assessing Return on Capital Employed.

Aggressive Acquisition Strategies

Companies that rely heavily on acquisitions to grow their business may exhibit artificially inflated ROCE figures. Using leverage and aggressive accounting practices related to acquisitions can distort the true profitability and efficiency of capital employed.

Poor Asset Utilization

Inefficient asset utilization can result in lower ROCE. Companies that struggle to optimize their assets, such as inventory, property, plant, and equipment, may experience reduced profitability and lower returns on their capital investments.

Unexplained Increase in Intangible Assets

A sudden and unexplained increase in intangible assets may warrant further investigation. Intangible assets, namely goodwill or intellectual property, can impact ROCE.

However, a significant and unexplained increase in intangible assets without corresponding improvements in profitability may raise concerns about the accuracy of reported Return on Capital Employed figures.

Identifying these red flags requires a comprehensive analysis of a company’s financial statements, disclosures, and underlying business fundamentals.

Let’s explore some strategies for detecting potential financial shenanigans.

Strategies for Detecting Financial Shenanigans

Investors can employ several strategies to identify potential financial shenanigans and ensure a more accurate assessment of ROCE.

Here are some approaches for detecting manipulation and assessing a company’s true financial health:

Analyzing Key Financial Ratios

In addition to ROCE, analyzing other key financial ratios can provide valuable insights. Ratios such as profit margins, liquidity, leverage, and cash flow ratios can help identify inconsistencies or anomalies that may indicate potential manipulation.

Conducting Comparative Analysis

Comparing a company’s financial performance with its industry peers and competitors can highlight deviations or discrepancies. Comparative analysis can reveal if a company’s reported Return on Capital Employed figures are consistent with industry norms and if its profitability and efficiency align with its peers.

Scrutinizing Cash Flow Statements

Analyzing a company’s cash flow statements can help identify discrepancies between reported profits and actual cash flows.

Cash flow analysis clarifies a company’s ability to generate cash from its operations and reveals any inconsistencies that may be masked in the income statement.

Reviewing Auditor’s Reports and Footnotes

Carefully reviewing auditors’ reports and footnotes in financial statements can provide additional insights.

These sections often contain important information about accounting policies, significant transactions, or potential risks.

Auditor’s reports may also highlight any concerns or limitations identified during the audit process.

By employing these strategies, investors can enhance their due diligence efforts and make more informed decisions when evaluating a company’s financial health and Return on Capital Employed.

Importance of Due Diligence in Evaluating ROCE

Due diligence is critical in evaluating a company’s financial performance, including its ROCE. Conducting thorough research, analyzing financial statements, scrutinizing disclosures, and assessing the overall business fundamentals are essential to due diligence.

Investors should ensure they can access reliable and accurate financial information, consider multiple data sources, and seek professional advice when necessary.

By conducting diligent research and analysis, investors can minimize the risk of falling victim to financial shenanigans and make sound investment decisions.

Conclusion

Return on Capital Employed is a powerful metric that enables companies to evaluate the profitability and efficiency of their capital investments.

By understanding ROCE, businesses can identify areas for improvement, optimize their operations, and make strategic decisions to enhance their financial performance.

However, it is essential to consider the limitations of Return on Capital Employed, such as the timing of cash flows, risk considerations, industry variations, macro factors, and the need for a comprehensive performance evaluation.

By overcoming these limitations and utilizing supplementary metrics, companies can gain a more accurate and holistic understanding of their financial performance.

Ultimately, by leveraging ROCE effectively, businesses can unleash the power of capital to drive sustainable growth and success.

FAQs (Frequently Asked Questions)

What is a good ROCE ratio?

A good ROCE ratio varies across industries. Generally, a ratio higher than the industry average is considered favourable. However, it is important to compare the ratio against industry peers and consider factors such as industry dynamics, risk profiles, and the company’s track record.

How does ROCE differ from ROI?

ROCE measures the profitability and efficiency of capital employed, while Return on Investment (ROI) measures the return generated on a specific investment. ROCE provides a broader assessment of overall capital efficiency, whereas ROI focuses on the performance of a particular investment.

Can ROCE be negative?

ROCE can be negative if the company’s operating profit is negative or the capital employed exceeds the operating profit. A negative ROCE indicates the company needs to generate more returns to cover the capital employed.

Is a higher ROCE always better?

While a higher ROCE is generally considered better, assessing the ratio in the industry context, risk profile, and the company’s track record is important. A high ROCE alone does not guarantee sustained success, as other factors, such as industry dynamics and macroeconomic conditions, can influence a company’s performance.

Can ROCE be used for comparing companies in different industries?

Comparing ROCE ratios across various sectors can be challenging due to industry-specific variations in capital requirements, business models, and profitability levels. It is important to consider industry dynamics, benchmarks, and other financial metrics to ensure accurate and meaningful comparisons.

What are some common challenges when interpreting ROCE ratios?

Interpreting ROCE ratios can be challenging due to industry variations, market conditions change, and capital structure differences. Considering these factors and conducting a comprehensive analysis is essential to draw accurate conclusions.

How can companies enhance their ROCE?

Companies can enhance their ROCE by improving operational efficiency, optimizing asset utilization, implementing effective working capital management practices, and aligning capital allocation decisions with projected ROCE.

How does ROCE differ from other financial metrics like ROE and ROA?

While ROCE considers debt and equity in the capital structure, ROE focuses solely on equity, and ROA measures the return on assets. ROCE provides a comprehensive view of profitability and efficiency by considering the entire capital employed.

How can ROCE help evaluate investment opportunities?

By calculating the expected ROCE for potential investments, businesses can assess each opportunity’s feasibility and potential profitability, aiding in making informed investment decisions.

How can companies overcome the limitation of ROCE, not considering the timing of cash flows?

Companies can overcome this limitation by analyzing cash flow patterns, assessing working capital management, and considering metrics such as cash flow return on investment (CFROI) or discounted cash flow analysis. These approaches provide a more nuanced understanding of a company’s financial health.

Are there alternative metrics to consider alongside ROCE for evaluating risk and return?

Yes, metrics such as Risk-Adjusted Return on Capital (RAROC), Economic Value Added (EVA), or Return on Invested Capital (ROIC) can complement ROCE by incorporating risk considerations. These metrics provide a more comprehensive assessment of risk and return dynamics.

Does ROCE capture all the factors influencing a company’s financial performance?

ROCE alone does not capture all the factors influencing financial performance. It primarily focuses on capital efficiency and profitability. Companies should consider a range of metrics and qualitative factors to obtain a holistic view of performance, including revenue growth, market share, customer satisfaction, and innovation.

How can ROCE help companies in different industries make better strategic decisions?

ROCE assists companies in evaluating the returns generated from their capital investments. By analyzing ROCE, companies can make informed decisions regarding resource allocation, project selection, and expansion strategies based on their industry’s dynamics.

How does ROCE influence investment decisions in capital-intensive industries?

ROCE provides insights into the efficiency and profitability of capital investments. In capital-intensive industries, ROCE plays a crucial role in evaluating the viability of projects, optimizing capital allocation, and mitigating investment risks.

Can ROCE be used to evaluate the performance of small businesses in various industries?

Yes, ROCE can be used to evaluate the performance of small businesses across industries. It helps assess the efficiency of capital utilization and the profitability of investments, regardless of a company’s size or scale of operations.

Disclaimer: This blog is solely for educational purposes. The securities/investments quoted here are not recommendatory. This is not an investment advisory. The blog is for information purposes only. Investments in the securities market are subject to market risks. Read all the related documents carefully before investing.

Past performance is not indicative of future returns. Please consider your specific investment requirements, risk tolerance, goal, time frame, risk and reward balance, and the cost associated with the investment before choosing a fund or designing a portfolio that suits your needs. The performance and returns of any investment portfolio can neither be predicted nor guaranteed.

The information provided in this article is solely the author/advertisers’ opinion and not investment advice – it is provided for educational purposes only. Using this, you agree that the information does not constitute any investment or financial instructions by Ace Equity Research and the team. Anyone wishing to invest should seek their own independent financial or professional advice. Do conduct your research along with registered financial advisors before making any investment decisions. Ace Equity Research and the team are not accountable for the investment views provided in the article.